The Corporate Illusion: Why Profitable Companies Run Out of Cash (And How to Fix It)

It is one of the most brutal paradoxes in corporate finance: a company can have record-breaking sales, highly celebratory board meetings, and soaring paper profits, yet still collapse into bankruptcy just weeks later.

Outside the financial realm, people assume profitability equals safety. But inside the world of corporate treasury, professionals live by a different, much more realistic rule: "Profit is an opinion, but cash is a fact."

If you are building a modern business, studying treasury management, or stepping into the corporate finance space, mastering operational liquidity management is the ultimate line of defense between rapid growth and sudden liquidation. Let’s look at why this paradox happens, the underlying financial metrics, and the global cash management strategies used by top organizations to fix it.

The Reality of "Solvent but Broke"

To understand how a highly successful company runs out of money, you have to look at a classic timing mismatch.

Imagine a multinational technology company, RDK Solutions, wins a massive, $10 million contract to build out a cloud network for a giant corporate client in Europe. On the income statement, the accounting report tracking revenues and expenses, the numbers look flawless. The sales team rings the victory bell, revenue is logged immediately, and on paper, the company is highly profitable.

But look at the fine print of the contract: 90-day payment terms.

This means that while the accountants log that $10 million right now based on accrual accounting principles, the physical cash, the actual dollars, won't hit the company's bank accounts for three full months.

Meanwhile, operational expenses do not wait. Software engineers expect their paychecks every two weeks. Landlords expect office rent on the first of the month. Third-party data centers demand utility payments immediately. None of these suppliers care about a signed contract or a paper profit line. They want cash.

If a company runs out of physical money to pay those immediate obligations, it faces a critical crisis known as liquidity risk. This is the danger of being "solvent but broke", having massive assets on paper, but zero cash to cover immediate liabilities.

The Liquidity Spectrum & Lacking Cash Visibility

To survive these timing gaps, financial leaders look at the balance sheet as a spectrum of liquidity. In treasury operations, liquidity is simply a measure of how quickly and easily an asset can be converted into cash to pay an immediate bill, without losing its value.

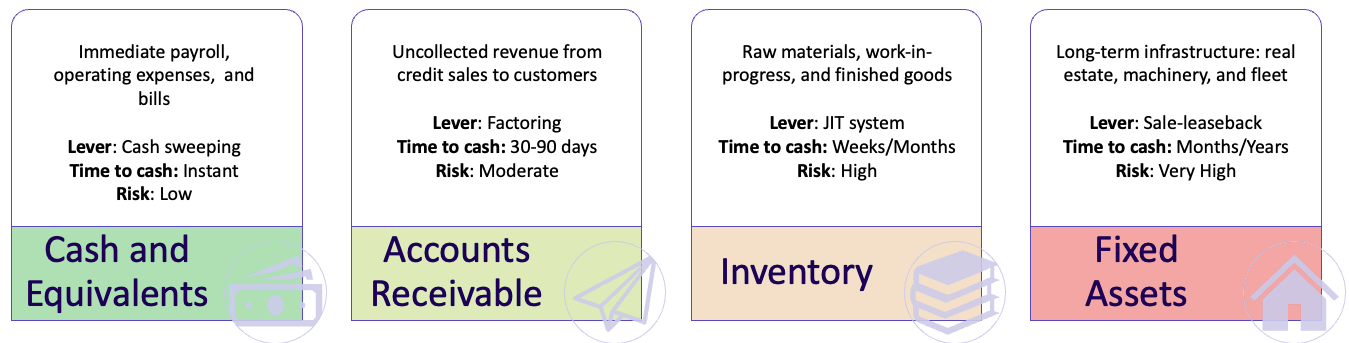

When analyzing liquidity, corporate treasurers categorize assets across a strict spectrum:

Cash and Cash Equivalents: Perfectly liquid. Money sitting in operating checking accounts can be wired to a supplier or payroll provider instantly.

Accounts Receivable: Moderately liquid. Funds owed by customers for completed sales. While they systematically convert to cash within standard payment terms (usually 30 to 90 days), you cannot use an outstanding invoice to settle a utility bill due this afternoon unless factored or discounted.

Inventory (Raw Materials/Finished Goods): Illiquid. If you suddenly need half a million dollars to cover payroll tomorrow afternoon, you cannot sell a warehouse full of tech components in a few hours without taking a massive financial hit.

Fixed Assets (Real Estate/Equipment): Highly illiquid. Selling physical corporate infrastructure takes months of legal and logistical processing.

Without real-time cash visibility across these tiers, a business is flying blind. A corporate treasury management team's primary mandate is to protect this cash runway, balancing long-term, illiquid investments with enough easily accessible cash to handle day-to-day survival.

How to Fix It: The Treasurer's Liquidity Toolkit

To prevent the "solvent but broke" paradox, corporate treasury teams deploy a strict toolkit of operational and financial strategies. Here are the four primary ways top-tier companies fix the liquidity gap.

Fix 1: The 13-Week Cash Flow Forecast (Visibility)

You cannot manage what you cannot see. While FP&A teams build 5-year strategic models, treasury teams build a highly tactical 13-Week Cash Flow Forecast.

Thirteen weeks perfectly equals one financial quarter. By mapping out exact cash inflows (customer payments) and outflows (payroll, rent, supplier invoices) over this horizon, the treasurer creates a financial radar system. If the forecast shows a $2 million cash deficit in Week 4 due to the 90-day contract delay, the company can prepare for it in Week 1, rather than panicking on payday.

Fix 2: Optimizing the Cash Conversion Cycle (Efficiency)

Where does this operational cash come from in the first place? It is generated by the operational heartbeat of the business, measured scientifically by the Cash Conversion Cycle (CCC). The CCC tracks the exact number of days corporate capital is trapped inside operations before turning back into cash receipts.

Treasury management teams optimize this cycle by adjusting three fundamental metrics:

CCC=DIO+DSO−DPO

Days Inventory Outstanding (DIO): The average number of days inventory sits on shelves before being sold.

Days Sales Outstanding (DSO): The average number of days it takes for customers to pay their invoices after a sale.

Days Payable Outstanding (DPO): The average number of days the company takes to pay its own suppliers.

If RDK Solutions takes 60 days to build and sell a product (DIO), waits 30 days for customer payment (DSO), and has 45 days to pay its vendors (DPO), its Cash Conversion Cycle is exactly 45 days (60+30−45=45). For those 45 days, the company experiences a "cash gap" that must be funded via cash reserves or bank lines of credit.

An elite treasury function works closely with operations to drive the CCC as close to zero (or even negative) as possible, speeding up collections (lowering DSO) and strategically extending vendor terms (raising DPO) to unlock millions in internal liquidity.

Fix 3: Cash Pooling & Bank Architecture (Centralization)

For expanding companies, cash management becomes even trickier because cash gets fragmented. When a company operates globally, it opens accounts everywhere - dollars in New York, euros in Frankfurt, yen in Tokyo. Before long, money is trapped in dozens of isolated corporate pockets worldwide, rendering global balances inefficient.

To smash this fragmentation and mobilize corporate funds, a modern treasury function deploys an optimized bank account architecture utilizing two primary cash pooling mechanisms:

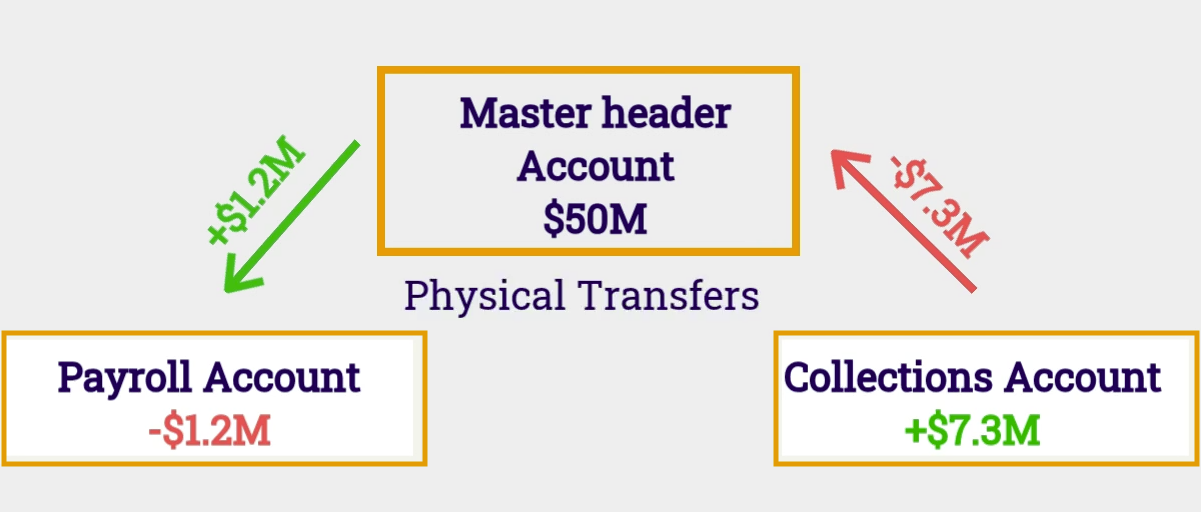

Zero-Balance Accounts (ZBA)

A ZBA structure physically connects regional operating accounts to a centralized master account. At the close of every business day, the partner bank automatically sweeps money back and forth to consolidate funds.

Zero-Balance Account (ZBA) Physical Sweeping Structure

As shown in the technical flow above, if a regional operating account experiences a deficit, the master account automatically funds it. If an account receives a customer payment, that entire amount is physically swept up to the master header account. The local accounts always reset to zero, achieving total cash centralization and eliminating idle balances.

Notional Pooling

What if cross-border regulations, tax hurdles, or high transaction costs make physically moving cash across borders impossible or illegal?

Treasurers use Notional Pooling. With this method, no physical cash is moved. The balances stay exactly where they are in their respective countries. Instead, the partner bank looks at all global accounts virtually, summing them up into a single net position.

If a subsidiary in Germany is short $400,000 and a subsidiary in France has an excess of $1 million, the bank virtually offsets them. The corporate entity avoids heavy overdraft fees and optimizes interest on the net position of positive $600,000 without triggering complex intercompany tax loans.

Notional Pooling structure

Fix 4: External Liquidity Nets (Funding)

If the timing gap is simply too large for internal optimization or pooling to cover, the treasurer fixes it using external financial instruments to bridge the divide:

Revolving Credit Facilities (Revolvers): Essentially a massive corporate credit card. The company draws down cash from a pre-approved bank line to cover immediate payroll, and repays it when the 90-day customer contract finally clears.

Invoice Factoring (Receivables Finance): Instead of waiting 90 days for that $10 million European contract to pay out, the company sells the invoice to a financial institution today for $9.8 million. The company takes a slight discount, but secures instant cash to keep operations alive.

Supply Chain Financing (Reverse Factoring): While regular factoring speeds up cash coming in, this tool optimizes cash going out. The company partners with a bank to pay its suppliers immediately. The supplier gets instant cash (minus a small bank fee), and the company pays the bank back 60 or 90 days later. This win-win eliminates supplier liquidity risk while allowing the company to hold onto its own cash much longer.

Final Takeaway: Reaching a "Real-Time Treasury"

Ultimately, elite working capital management is about eliminating financial blind spots.

Accounting tells you how healthy a business was. Financial Planning (FP&A) models how healthy it could be. But a strong cash flow forecasting process ensures the business survives today so it actually has a chance to reach that future.

By mapping the liquidity spectrum, tracking the cash conversion cycle, and centralizing global banking pipelines, financial leaders stop playing defense and turn cash efficiency into a launchpad for global expansion.

Enjoyed this breakdown? This article is the first of a series unpacking the hidden mechanics of global corporate finance and treasury management trends. Let me know your thoughts or questions on liquidity risk management in the comments below!